While conventional loans often require 5-20% down, qualified veterans can purchase a home with zero money down. That means you can stop waiting and start owning.

Most lenders require PMI if you put down less than 20%, adding hundreds to your monthly payment. VA loans eliminate this requirement entirely, keeping more money in your pocket each month.

VA loans typically offer lower interest rates than conventional mortgages. Over a 30-year loan, this can translate to tens of thousands in savings.

Your credit score doesn't have to be perfect. VA loans offer more lenient requirements than conventional mortgages, opening the door for veterans who might not qualify elsewhere.

Sellers can contribute up to 4% of the home's value toward your closing costs, reducing what you need to bring to the table.

Buying a home should feel like a milestone, not a marathon. We help first-time and repeat buyers navigate the VA loan process with confidence. Our network of VA approved lenders understands the unique requirements of VA financing and will guide you from pre-approval through closing day.

Already have a VA loan? The IRRRL (also called a VA Streamline Refinance) helps you lower your interest rate and reduce your monthly payment with minimal paperwork. It's one of the fastest, simplest refinance options available.

Your home equity is a financial tool. A VA Cash-Out Refinance lets you tap into that equity to consolidate debt, fund home improvements, or cover major expenses, all while potentially securing a better rate.

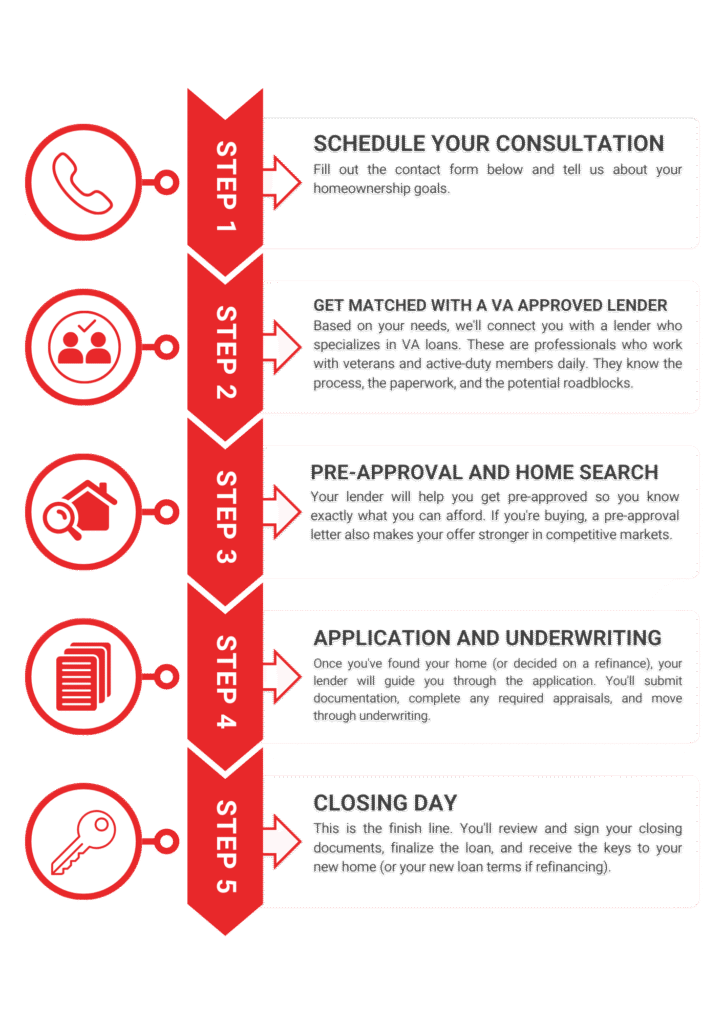

Fill out the contact form below and tell us about your homeownership goals.

Most lenders require PMI if you put down less than 20%, adding hundreds to your monthly payment. VA loans eliminate this requirement entirely, keeping more money in your pocket each month.

Your lender will help you get pre-approved so you know exactly what you can afford. If you're buying, a pre-approval letter also makes your offer stronger in competitive markets.

Once you've found your home (or decided on a refinance), your lender will guide you through the application. You'll submit documentation, complete any required appraisals, and move through underwriting.

This is the finish line. You'll review and sign your closing documents, finalize the loan, and receive the keys to your new home (or your new loan terms if refinancing).